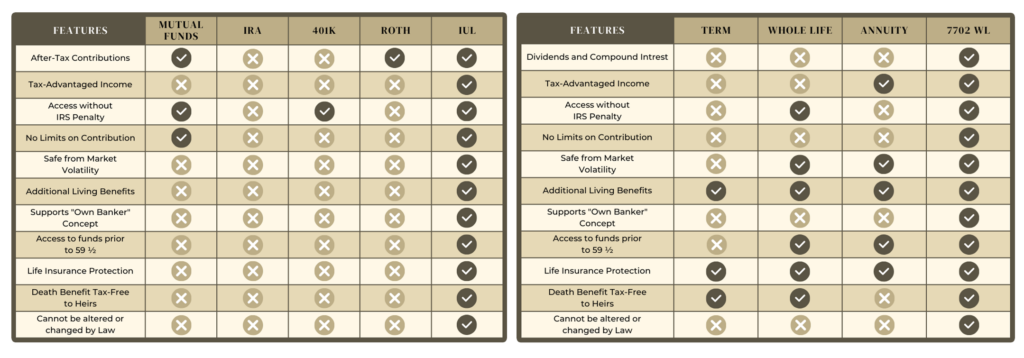

Planning for a tax-free retirement is an attractive option for those seeking to maximize their retirement savings. Take a look at some of the most common tax-free retirement options below to learn more about what suits you best!

Indexed Universal life insurance (IUL) is a flexible premium permanent life insurance product that credits interest to either a fixed account and/or an index-linked account option. Funds allocated to the index-linked account have a crediting rate that is based on the performance of a market index, such as the Standard & Poor’s 500 (S&P 500) price index.

The premium is paid to the insurance carrier. A portion of the premium is used to cover the policy expenses and the cost of insurance. The remaining premium, the net premium, is eligible to be placed into the interest-bearing account. Interest, if any is credited to the policy account, increasing the account value. The account value is then available for policy expense coverage or reinvestment.

Account values enjoy the upside potential of the stock market based on changes in the securities indices chosen and may experience downside protection in the form of a minimum guaranteed interest rate commonly referred to as the “floor”. The floor is a rate that is set, typically the rate will never be less than 0%, but could be more. However, floors do not account for policy charges, so the account value of the policy could decrease even with a floor. Therefore, an IUL policy can lapse if there is insufficient value to cover the policy charges even if premiums have been paid as planned.

If you’re looking to supplement your retirement income of guarantee income for the rest of your life, an annuity might be a smart choice for you. Annuities are contracts between an individual and an insurance company in which the individual pays a lump sum or a series of payments in exchange for a guaranteed stream of income over a period of time. Annuities are one of the few sources of retirement income that can guarantee* income for life. (*Guarantees are based on the claims paying ability of the issuing company). They are designed to help you accumulate funds for a long-term goal, like retirement, and/or protect you from the risk of outliving your savings.

An immediate annuity is a type of annuity contract for those with immediate income needs in which there is a single, lump-sum purchase payment, and periodic payments can help provide income, generally within a year of the purchase of the annuity. It is important to note that immediate annuities have limited liquidity.

A deferred fixed annuity is an annuity contract that allows an individual to receive payments at a future date. It has an accumulation phase between the date the contract is issued and the date you begin receiving income payments. During this phase, your funds have the potential for growth depending on the type of annuity purchased. It offers a guaranteed interest rate, tax deferred growth and principal protection.

The simplest form of an annuity, a fixed annuity, starts out providing a guaranteed interest rate, typically for a guaranteed period, while also providing protection of principal. After the guarantee period ends or at the contract’s latest permitted annuity date, the annuity can be turned into a stream of guaranteed income for a period of time and/or a person’s lifetime.

A variable annuity lets the annuitant receive larger or smaller payments in the future depending on how well the investments of the annuity fund do.

With Whole Life Insurance, you’re guaranteed1 a death benefit, and you’re able to build cash value over time. Your cash value grows tax deferred so it’s there when you need it.2 In addition, with Participating Whole Life Insurance, eligible participating policyholders have the opportunity to earn dividends3, which are not guaranteed.

1 Guarantees are based on the claims paying ability of the issuing company or companies.

2 Access to cash values through borrowing or partial surrenders will reduce the policy’s cash value and death benefit, increase the chance the policy will lapse, and may result in a tax liability if the policy terminates before the death of the insured.

3 Dividends are not guaranteed.

7702(j) accounts are not actually retirement accounts, but a tax code that allows you to utilize Participating Whole Life and IUL (Indexed Universal Life) policies that allows policyholders to accumulate tax-deferred savings that can be used for retirement income. These policies offer some unique features, such as tax-free withdrawals in retirement, a cash value component, and a death benefit for your beneficiaries that is funded by overpayments.

A tax-advantaged retirement strategy, is designed to help you maximize your savings and minimize your tax burden in retirement. Don’t miss out on this opportunity to have a tax-advantaged retirement solution – contact us today to learn more about how we can help you!